Should Inflation > Deflation, still?

Does inflation still hold up to the national enemy of deflation?

*This letter will be US-economy-focused. It aims to shed clarity on whether the inflation-driven approach to policy has been worth its trade-offs.

The ultimate economic goal is as follows: To produce more useful stuff with time. Useful stuff refers to goods & services that when consumed, give utility to their consumers.

We humans have designed a number of measurements to help us deduce how the economy is doing. These measurements have served as metrics on top of which goals can be set. Within a closed system, the most notable measurements are the following:

Real output (expansion or recession?)

Unemployment rates (low or high?)

Price levels (inflation or deflation?)

For decades, the US government has focused on making these measurements “tilt” in a specific direction.

This is best exemplified by the dual mandate of the Fed: keep unemployment as low as possible and ensure low and stable inflation; In line with conventional wisdom: growth in real output is good, lower unemployment is good, and deflation is very bad.

Except, the direction of the “tilt” is not by itself indicative of good or bad.

Conventional wisdom is not wrong. But as we’ll soon see, it’s full of blanket statements that oversimplify.

Depending on the context,

An economy growing at 2% can be equally effective at achieving the ultimate goal as an economy shrinking at 2%. An economy with an unemployment rate of 5% may be more in line with the ultimate goal than an economy with an unemployment rate of 0%. And an economy with 2% inflation may be much less effective than an economy with 2% deflation.

Let’s explore why such may be the case using some simple (and exaggerated) analogies:

Expansions vs Recessions

One day, everyone comes to the sudden conclusion that we have too many fidget spinners around and that nobody really wants them anymore. Demand for spinners falls. Temporarily, the people who were making money from selling spinners stop making money. Workers at factories producing these spinners get unemployed. For a period, net produce of the economy falls — because fidget spinners just suffered a massive hit. We have a recession.

Is this a bad thing? On aggregate, no. It is simply an adjustment; Such an adjustment may be slow, or it may be fast. But eventually, resources that were being wasted on producing spinners will be allocated towards the production of something else.

We certainly don’t want a case where resources are being channeled towards the production of useless stuff. Though that may reflect on paper as an expansion, it doesn’t bring much value to the inhabitants of the economy.

Low vs High Unemployment

Technology displaces people when people don’t possess the skills required for the evolving economy. Unemployment rates increase. This is commonly referred to as technological unemployment.

Is this a bad thing? Not necessarily. (Though it would be good to help ensure that people have the access to the resources that can get them employed in emerging areas.) It’s an adjustment process.

And we wouldn’t want to hinder this process either — we certainly don’t want paper-servicing, where we give these people “jobs” to reflect their status as “employed”. Because at that point in time, they may just not have the capacity to contribute genuine value to the economy. (Going off tangent here, but this is an emerging narrative that’s worrisome.)

Inflation vs Deflation

Theoretically, this is the most straightforward dichotomy to resolve. Textbook economics actually embraces the narrative that both inflation and deflation can be good, depending on their causes. If productivity leads to deflation, the economy can produce more using less. Alternatively, if growing demand leads to inflation, people are encouraged to spend which in turn leads to more growth.

Supply-driven deflation is generally considered good, whereas demand-driven inflation is generally considered bad.

Zooming in on Inflation vs Deflation

We’ve understood why the direction of the tilt is by itself not indicative of good or bad. But we can make a judgement based on prevailing conditions in the economy and opine the direction in which a measurement ought to be tilting towards at that point in time.

Today, inflation is the headline: it’s hitting near-40-year highs. So it’s timely to zoom into it. As such, this letter shall focus on the measurement of price levels.

Much of the urge to inflate came from the fear of deflation. The fear of a tilt being in the wrong direction.

There’s plenty of debate surrounding inflation versus deflation. A look at the comments on the tweet below will give you a taste.

But to really find the answer to whether inflation or deflation is better suited for our prosperity in the new economic order, let’s look to the past to understand whether this sustained fear of deflation is warranted.

A bit of History

Conventional wisdom states that “inflation is good, and deflation is bad”, but such wasn’t always conventional. In fact, if viewed from a historical lens, such a narrative would probably be considered quite odd. Deflation used to be as common as inflation.

During the 2nd Industrial Revolution of the late 19th Century, deflation accompanied rising real wages. The same applied in the 1920s, where new “high tech” industries like automobiles and refrigerators proliferated.

For more examples of deflation during prosperous times, I highly recommend checking out this working paper. But as a summary:

In history, deflation has often coincided with robust economic growth. This is in sharp contrast to the conventional wisdom that generally is drawn from a more limited focus on deflation in Japan in the 1990s and deflation episodes in the Great Depression.

…

To an observer looking at the long history, current concerns about deflation may seem to be somewhat overblown. It is abundantly clear that deflation need not be associated with recessions, depressions, crises, and other unpleasant conditions. The historical record is replete with good deflations. There are, of course, plenty of bad deflations, too.

- Deflation in a historical perspective, Bank for International Settlements

So… Fears over deflation: Fair or misguided?

We tend to think of deflation itself as an illness. There is indeed some logic behind this: with deflation, people put off purchases and postpone spending. Debt becomes heavier for those who owe money. Borrowing becomes more expensive. And so on.

Such concerns are valid, but they don’t paint a complete picture. Deflation can indeed be an illness. But it could also be a by-product of other (good) phenomena happening in the economy. As previously mentioned: supply-led deflation can increase the limits of what a country can produce. If employees become more productive, a firm can produce more in the same 5-day work week. Technology can enable the same. These are reasons to be optimistic and confident about future economic performance — and they could very well counter the urge to postpone spending.

Therefore as an economic idea, we would be right to say that deflation receives excessive dislike.

But whether given conditions of today’s age, fears of deflation are justified warrants deeper analysis. Remember, neither deflation nor inflation is inherently good or bad — it really depends on context.

Consider context in determining whether to aim for inflation, or deflation.

Both inflation and deflation have their trade-offs; Neither is perfect. Part of the reason economists fear even supply-driven deflation is because should it be interpreted as demand-driven, it could go on to cause recessions.

We’ll approach the analysis in this manner:

First, we’ll examine whether inflation or deflation would occur based on today’s persistent and dominant free-market forces. What trade-offs would arise due to that inflation or deflation?

Next, we’ll consider what would have to be done to reverse that trend, assuming governments deem it inappropriate. What trade-offs would arise from those interventions?

Finally, we’ll compare the two scenarios and determine which is less problematic on the aggregate.

This may seem like a false dichotomy between a free-market economy and one with a notable degree of government intervention. But bear with me! — things will get less foggy soon. Condensing this idea will reveal what’s at the heart of the question on whether to inflate, or deflate.

1. The Free Market Result & its Implications

The natural force that’s Technology

The dominant natural force driving the direction of price levels is technology, which is deflationary for numerous reasons: goods and services can be scaled more efficiently, new services are created by nascent technologies, and the same output can be derived from inputting less. A famous example is how streaming services drastically reduced the cost of media consumption (consider the cost of a Netflix subscription today versus buying a DVD years ago).

Technology is deflationary. That is not conjecture. It is the nature of technology. And because technology underpins more and more of the world around us, it means that we are entering into an age of deflation unlike any the world has ever seen.

…

Technology is moving too fast — and it will only move faster from here. Even if we wanted to, we can’t put the genie back into the bottle.

- The Price of Tomorrow by Jeff Booth

Technology will deflate more and more industries with time. If you’re interested, I highly recommend reading this piece which makes a compelling case for why technology-driven deflation is here to stay.

There are other aspects to the supply-side of the argument — one example being evolving education. But let’s focus on the dominant pieces that we can be certain about; Technology is the one dominant player whom we can be very certain about.

But even tech-driven deflation may entail certain trade-offs.

Trade-offs from tech-driven deflation

Firstly, people may hoard their money due to the deflation.

It may improve real output, but it may also slow down the growth of aggregate demand in the economy if people hoard their money. However, this is unlikely to be a concern if labor is adapting to technology and people recognize that the deflation is tech-driven. It’s an opportunity and we can be cumulatively better off. In which case, an improvement in consumer confidence and market sentiment will boost aggregate demand anyway. So this trade-off may not be a significant one.

Secondly, people may misinterpret this supply-led deflation as demand-driven.

The “deflation is bad” story has been strongly instilled. So it’s possible that people may wrongly interpret tech-driven deflation as demand-driven deflation. In which case paradoxically, tech-driven deflation may decrease aggregate demand. But this argument is also dubious because many forces are involved. Prominent economists could come on television and say it’s supply-driven. People may see things getting cheaper while their wages stay still. Point is: the interpretation problem is unlikely to sustain itself.

Third, debt gets harder to pay off and borrowing is harder.

We’ll be discussing the public debt side of the equation later. But with respect to private debt, though this could damage aggregate demand, private debt becoming less attractive may not be a bad thing. House of Debt well outlines why:

A financial system that thrives on the massive use of debt by households does exactly what we don’t want it to do — it concentrates risk squarely on the debtor.

…

The concentration of losses on debtors is inextricably linked to wealth inequality.

…

Even households in the economy that stayed away from toxic debt during the boom suffer the consequences of the collapse in household spending during the bust.

- Princeton Economist Atif Mian and UChicago Economist Amir Sufi

The US — as it is — has a borrowing and debt problem, on both the public and private front. It’s a recipe for disaster. There are many economies doing even better that don’t have a debt problem. Prospering without debt is possible.

So why deflation on debt may cause short to medium-term pain, it may not be a bad thing. Hence, this trade-off is not an overbearing concern.

The demand-side forces of outlook

By outlook, we’re referring to consumer confidence and market sentiments.

I would argue that the demand-side of the equation should not be a key determinant of whether deflation or inflation should be the goal of the new economic order. It is constantly fluctuating. These characteristics are not persistent.

We’ll touch on this later. Oh, and if you’re looking for the impacts of the Russian Invasion or Covid-19, we’ll touch on those later, too. Let’s move on for now.

Verdict for Part 1

Technology is the key persistent and dominant force that will continue to characterize the new economic order. And since technology is deflationary, the free-market product would be deflation.

We’ve made it clear that even tech-driven deflation is mostly fine — even its trade-offs don’t raise too many eyebrows. But can the inflationary alternative do even better?

2. Intervening for inflation and its implications

The persistent and dominant forces from intervention driving the direction of price levels are the following: expansion in broad money supply and the low cost of borrowing.

With the Russian invasion of Ukraine coming right after Covid-19, it may seem odd that “Supply Chain Issues” isn’t part of the list above. But we’ll touch on this later. Oh, and please, to clarify: corporate greed is not a strong reason:

Expansion of Broad Money Supply & Low Cost of Borrowing

Both of these factors are mutually reinforcing. Billionaire investor Ray Dalio explains why:

“Throughout history, rulers have run up debts that won’t come due until long after their own reigns are over, leaving it to their successors to pay the bill. Printing money and buying financial assets (mostly bonds) holds interest rates down, which stimulates borrowing and buying. Those investors holding bonds are encouraged to sell them. The low interest rates also encourage investors, businesses, and individuals to borrow and invest in higher-returning assets, getting what they want through monthly payments they can afford.”

- Ray Dalio, The Changing World Order: Why Nations Succeed and Fail

This is a persistent and dominant force in recent American history. It’s not just a “during a crisis” thing. (Although certainly such shocks have resulted in more credit expansion and even lower interest rates.)

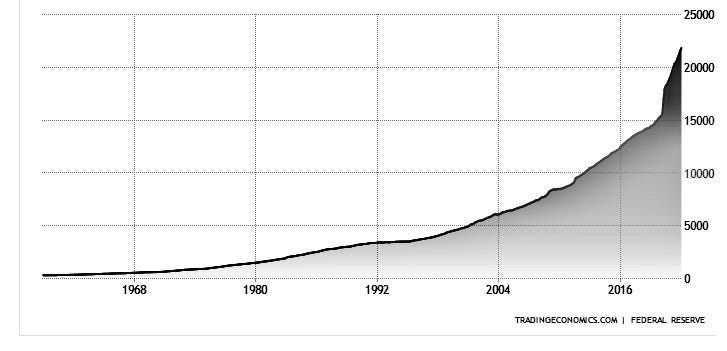

Here’s some evidence to warrant the above claim:

Based on the blue chart below, we can infer that base money supply has been increasing at a faster rate as a whole. More base expansion opens up the opportunity for further broad expansion. So long story short: the “printing” is here to stay.

(For those unfamiliar with base vs broad money, I highly recommend checking this article out.)

The printing aimed to do good. During disasters, its rationale is move obvious — injecting money stimulates falling demand so that we don’t get a recession on paper. During more normal times, should an economy be deemed to require huge levels of debt to keep functioning, printing may be warranted, too.

But given its trade-offs, is it worth it?

Trade-offs from Broad Money Supply Expansion (aka Money Printing)

Firstly, debt-driven growth can lead to currency debasement. This will end with a massive crash.

Having a reserve currency is great while it lasts because it gives a country exceptional borrowing and spending power and significant power over who else in the world gets the money and credit needed to buy and sell internationally. However, having a reserve currency typically sows the seeds of a country ceasing to be a reserve currency country. That is because it allows the country to borrow more than it could otherwise afford to borrow, and the creation of lots of money and credit to service the debt debases the value of the currency and causes the loss of its status as a reserve currency.

- Ray Dalio, The Changing World Order: Why Nations Succeed and Fail

The US is way past that point where it can pay back its debt. There’s been extensive literature on this. (I think this article is a great summary.) But the bottom-line is: debasement of the US dollar is already happening. Central Banks are accelerating their shift from dollars to gold worldwide. The share of USD held by foreign exchange reserves dropped to a 25-year low mid-last year. The Chinese Yuan (or Renmibi, if you want to be precise) and Euro still have a long way to go before catching up to the dollar, but the catch-up is happening; And if people get worried fast enough, the catch-up will happen even faster.

Being the reserve currency has its pros and cons for the USD, but the cons are quite negligible because they apply largely assuming that supply of USD remains stable — which is obviously not the case. And so right now, unequivocally: reserve currency status is major bonus for the USD. And the trade-offs from expanding broad money supply are huge.

Another problem is that such sustained credit expansion itself creates further inflation expectations. Many say that QE shouldn’t be blamed for the inflation — for example, Paul Krugman often describes that it isn’t credit expansion that’s the problem, but rather inflation getting entrenched in expectations.

But again, these aren’t disconnected factors — People are understandably confused about what’s going on. So policies like QE and YCC will understandably raise fears about future inflation. And that fear will feed on itself. These are still symptoms of credit-expansion policies.

“There’s a real risk now that… inflation may be more persistent and that may be putting inflation expectations under pressure,”

- Fed Chair Powell, December 2021

Lastly, given the direction debt is going, it’s driving up inequality with it.

This is because intervention in the economy via public debt (the majority of the debt) is systemically designed to go through financial institutions and help asset holder first — i.e. richer people. The trickle-down effect is not at all apparent. Here’s a super cool 40-year chart from researchers at UC Berkeley — tracking inequality and income in real time:

And so the trade-offs from pursuing inflation via debt-fuelling credit-expansion are very significant.

Verdict for Part 2

The cost of pursuing inflation has been tremendous because most of it has come from huge credit expansion — expansion so huge it can cover the compounding deflation of today’s technology.

Why not consider Russia, or Covid?

These are both huge shocks (and tragedies). But they are still temporary and the economy will recalibrate.

These may be dominant forces at this point in time, but it will not persist. Remember: it is the dominant and persistent forces that we have to pay the closest attention to. This isn’t to say that the nature of supply chains won’t intrinsically change — but they will stabilize, even if that means having deglobalization and regionalisation, or a new global order.

3. The Big Verdict

Both tilts have their trade-offs. But given today’s context,

Deflation > Inflation.

The trade-offs of turning the natural deflation into inflation are massive. In comparison, the trade-offs from deflation are minuscule.

This is not saying “Government shouldn’t intervene!” — we don’t want to pose a false dichotomy. But intervening to keep inflation going is not worth it.

We’ve tried to navigate through some big questions in this letter. And consequently, opened up bigger ones, too. The most notable ones being: how would transitioning to a deflationary system even look like and what would be the costs of that transition?

But that’s for another day.

Till then,

Ja ne!

I created this newsletter to share, get roasted, and learn along the way. So if there’s anything you feel that I got wrong, or you’ve feedback in general, do let me know in the comments or DM me on Twitter!

P.S. This is not financial advice! Let’s all think with our own heads!

Some questions left unexplored:

Is postponing spending really a bad thing? Answering this question requires us to examine time preference, which we will do in future letters.

If deflation > Inflation, what degree should we be aiming for? Will we even have a choice?

If it’s too late for the US to turn back, what’s going to be the next global reserve currency?

Some image references:

https://courses.lumenlearning.com/suny-macroeconomics/chapter/shifts-in-aggregate-supply/

http://clipart-library.com/clipart/rTjRxryTR.htm

https://commons.wikimedia.org/wiki/File:US_Historical_Inflation_Ancient.svg