Corporate Power isn't driving inflation. Here's why.

A letter to Matt Stoller and Robert Reich

A quick summary:

Big personalities are pushing that corporate power/concentration is DRIVING inflation today.

Some even posit that it is the BIGGEST inflation driver: e.g. Matt Stoller, who released an article on how corporate profits, from corporate power, were driving 60% of current inflation.

But corporate power hasn’t increased since the pandemic, whereas inflation has. So corporate power is definitely not the SOURCE.

It may be a COMPOUNDING FORCE that worsens the inflationary effects of money printing or supply chain issues, though.

But how STRONG a compounding force is it?

We explore this question by examining whether corporate profits are indeed driving 60% of inflation.

The answer to that is NO. In fact, nowhere near. Notably, Stoller’s math forgets that companies export and how CPI is computed — it wildly understates price increases.

The influence of corporate power is closer to 0% than to 60%.

Now, let’s dive deeper.

Hey everyone,

At the end of 2021, author and Harvard alumnus Matt Stoller ran some numbers and concluded that corporate profits were driving 60% of inflation. He reckoned that corporate profits, as a result of corporate power, was the BIGGEST inflation driver.

Robert Reich has argued for the same. Most recently, he released a Youtube video on the topic which has over a hundred-thousand views.

Inflation hasn’t settled down since, and the solution these folks propose is the reduction of corporate power i.e. improving antitrust laws so that firms compete against each other and drive down prices.

This letter will focus on applying Stoller’s mathematical framework to compute a more accurate value reflecting corporate power’s influence in driving inflation.

Quick clarification: Corporate power can be a compounding force that worsens inflation, but it’s no SOURCE.

The argument for corporate power being a driver of inflation is simple and also admittedly intuitive: Cost pressures from stressed supply chains wouldn’t be such a big problem if we didn’t have corporate power as a massive compounding force. Because then, firms would be forced to absorb these price increases. Consumers would still see their groceries getting more expensive, but not to this degree.

However, though corporate power may have worsened inflation during the pandemic, corporate power was not the source of inflation.

This is for the simple reason that corporate power has not increased significantly since the start of the pandemic, whereas inflation clearly has.

Stoller does reference Summers’ thread in his letter, but it isn’t clear how his reasoning, comprised primarily of odd math and the words of a couple of Wall Street folks, rebuts it.

Regardless, his conclusion is clear: corporate power is worsening inflation. He then proceeds to answer the next key question:

How significant is corporate power in driving inflation?

Stoller makes a powerful point: if we had less corporate power, we’d be seeing 60% less inflation. That’s a lot less.

At this juncture, I urge you to read his article.

Stoller ends up at the “60%” through some interesting math. He clarified that these are back of the envelope calculations, but I worry that their margin of error is more significant than suggested. Let’s go step by step.

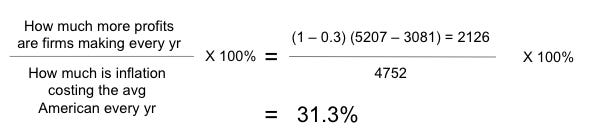

Firstly, he wants to find out how significant the increase in profits for American non-financial corporations is, relative to the costs of inflation. In other words, how much of your costs are coming from firms increasing their prices, to increase their profits, just because they can? He arrives at 44.7%.

The first problem in this step is that American Companies don’t make profits solely from selling to Americans. They sell overseas, too. According to the framework Stoller has set, we ought to be considering how much more profits firms are making in America only.

By his logic, greedy corporations would be raising prices in any country facing inflation, using the same inflation as an excuse. Key export avenues like Europe and Canada are also facing worsening inflation.

Using the example of PepsiCo, a firm Reich bashed for increasing prices using inflation as an excuse, we can see that about 40% of PepsiCo’s revenue comes from outside the US. 30% comes from markets like Europe and Canada. P&G, another firm Reich bashed, has over 50% of its revenue coming from outside the US, concentrated in Europe and Canada, too.

Ultimately, taking reference to how US exports are broken down by country, let’s assume that 30% of exports go to inflationary avenues like Canada and Europe. Once we take into account the fact that profits come from overseas, too, the number 44.7% drops to 31.3%:

He also uses CPI to calculate how much inflation is costing the average American in. This is problematic because CPI understates the year on year increase in prices.

I highly recommend this video to better find out why. But here’s a primer:

Over the years, the methodology used to calculate the CPI has undergone numerous revisions. According to the BLS, the changes removed biases that caused the CPI to overstate the inflation rate. The new methodology takes into account changes in the quality of goods and substitution. Substitution, the change in purchases by consumers in response to price changes, changes the relative weighting of the goods in the basket. The overall result tends to be a lower CPI.

For example, this means that if a car manufacturer with corporate power doubles a car’s price from $30k to $60k and the government deems that there has been an equivalent double in “quality” — a completely subjective judgement — the CPI will report a 0% value based on that good. Not 100% as you may have expected. Pretty big difference. The manufacturer’s profits just shot up but… this wasn’t reflected in the CPI at all.

To find out how much inflation is costing the average American yearly, we’d be better off examining CPI calculated based on the government’s metrics in the 1970s. Using those metrics, conservatively, current CPI would stand at about 15%. Based on that, the 31.3% calculated previously undergoes a further reduction to 14.2%:

Now, this means that increased profits from corporate America comprise of just 14.2% of the inflationary increase in costs.

Following through on his methodology, this further means that corporate profits alone are absorbing 2.1% % inflation rate on all goods and services in America (14.2% of the 15% annual inflation).

If you take the pre-existing inflation rate in 2019, as per the 1970s CPI metric, when inflation was about 8%, and back that out of the numbers… it turns out that 30% of the increase in inflation is going to corporate profits. A pretty big difference from the 60% quoted.

Hence, following through on his methodology:

Corporate power, and thereby profits, is driving 30% of inflation. Not 60%.

By the way, if you had a problem with me using the 1970s CPI, the final number would still fall to 44.3% from the 60% quoted. Purely from recalling that American companies export.

This entire methodology is flawed, and an accurate value is impossible.

This way of calculating how much corporate power influences inflation has innate flaws.

Most notably, it discounts demand changes. Consumption patterns change, and demand shifts. Remember: a lot of money was created during this pandemic to stimulate demand. It’s very odd to ignore demand in a period where the government essentially created the most amount of credit ever.

Sadly, Stoller’s methodology makes a one-to-one comparison where one doesn’t exist. The only real way to compute the significance of corporate power in compounding current inflation would be to compare the increase in prices now, to the increase in prices in a hypothetical scenario where corporate power was lower. Unfortunately, there’s no practical method to do so.

It’s dangerous to make one genuine problem a distraction from another.

I understand that Reich and Stoller are passionate about reducing corporate power, and it’s an admirable cause. I agree that corporate power is a very real problem: innovation is getting stifled, prices are unnecessarily high, and so on.

But their links between inflation and corporate power appear exaggerated. And blaming corporate power for everything won’t help. So let’s not get distracted.

I hope you enjoyed reading this letter, and I’ll be back next week.

But till then,

Ja ne!

P.S. I created this newsletter to share, get roasted, and learn along the way. So if there’s anything you feel that I got wrong, or you’ve feedback in general, do let me know in the comments or DM me on Twitter!

Image references:

Agree. This is the problem with ideology driven agenda. If you only have a hammer, every problem looks like a nail! While monopoly/ corporate pricing power is a concern, far bigger problems drive inflation and USA is at an inflection point / cross roads. Focusing on distractions like corporate pricing power is a very bad idea!

Was a good read! You have brought up very valid points